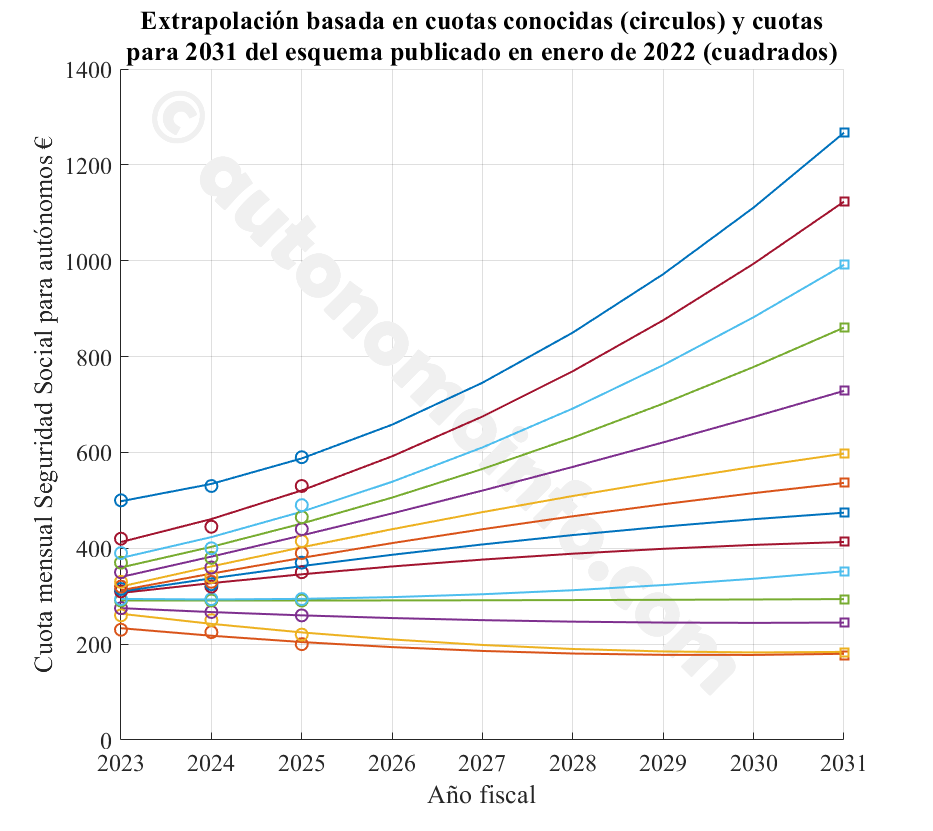

How we estimate the quotas for 2026-2031

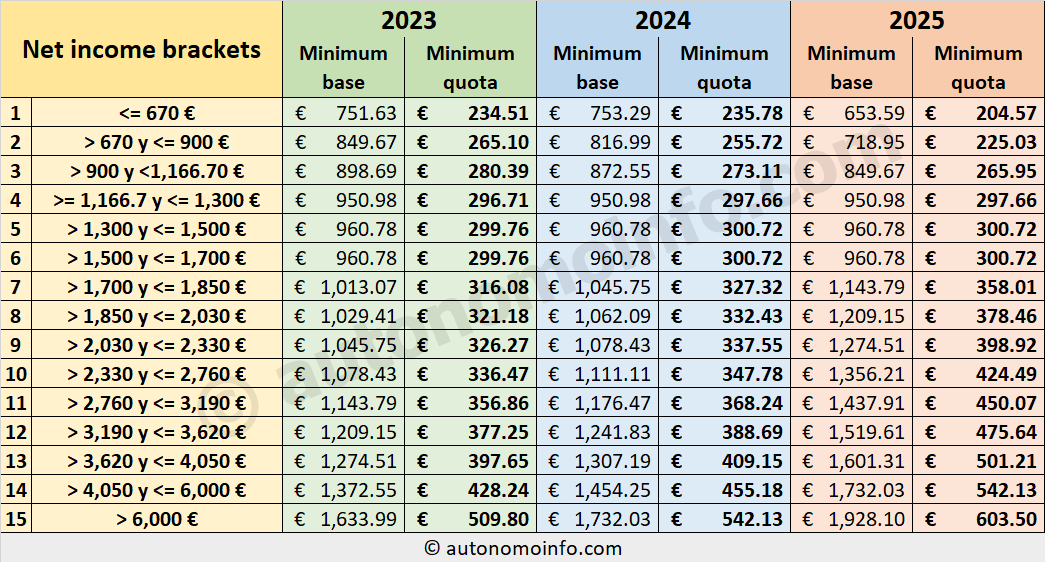

In 2022, the Spanish government set in motion a scheme to gradually increase the social security payments for self-employed over a transitional period of 9 years from 2023 to 2031. For now, the government has only published the new quotas for the years 2023-2025, while the values for the following years will not be known until 2025. Nevertheless, our calculator allows you to use fiscal years up until 2031, the last year of the transition period. Below we explain how this was achieved.Before the current scheme was approved, the government already indicated how they would like to increase the contributions until 2031 and the proposed scheme was published in an article in el País. While this scheme has since been replaced, it nonetheless provides an indication of where the government would like to be by the end of the transition period in 2031. So, to estimate the contributions for the years from 2026-2031, we used the quotas for the years already known (2023-2025), added the endpoints (2031) from the scheme in the el País article, and applied a least squares regression (best fit) of a second order polynomial to obtain the intermediate years 2026-2030. The result is shown below.

Clearly, these are highly speculative at this point and are only meant to provide an indication of where things might be headed after 2025...

Calculate your income tax and new social security contributions from 2023 onward as a self-employed in Spain

Click for more info on the Spanish self-employed system

Use this tool to calculate how much you have to pay in social security contributions and income tax with the new self-employed scheme introduced in Spain in 2023 and see how this affects your net income compared to the old scheme.