Self-employed vs Limited Company: A Closer Look

For many self-employed professionals, there comes a point at which they wonder whether transitioning to a limited company might be the better option, particularly after achieving sustained business success. Many online resources, often published by Spanish accounting firms, recommend making this shift once earnings reach the €40,000–€60,000 range. However, it is worth taking a closer look, as these recommendations may not be free from commercial bias: accountancy firms naturally have an interest in helping you set up a company and subsequently managing your bookkeeping and tax affairs.

What does it mean to have a company in Spain?

Before comparing the freelancer and limited company models side by side, it is useful to clarify what establishing a limited company in Spain actually involves.

Company formation

For a self-employed professional, the legal entity that would typically apply when forming a company is a so-called Sociedad Limitada Unipersonal — a single-member limited liability company, abbreviated as S.L.U. Forming a company in Spain is relatively cumbersome compared with other parts of the world, although formation times have improved significantly: what could take up to 28 days only a few years ago can now be completed in as little as 4 days through specialized companies. These providers may charge anything from around €250 to four-figure amounts, depending on the complexity of the formation process, for example if customized company statutes are required.

Although many steps in the formation process can now be completed online, you will still need to visit — and pay — a notary in person, as well as open a company bank account. Typically, if you own and work in your company, you will remain in the Spanish self-employed social security regime (RETA), but as an autónomo societario. This does not mean that the tax and social security treatment is identical to that of a regular autónomo. Under the post-2023 income-based contribution system, the RETA contribution base for an autónomo societario can take into account remuneration received from the company and also capital income, including dividends derived from the shareholder’s participation in the company. A 3% generic expense adjustment is applied for certain company owners, compared with the general 7% adjustment used in the RETA calculation for regular autónomos. This is separate from the IRPF deduction for gastos de difícil justificación, which is 5% capped at €2,000 for regular autónomos under simplified direct estimation.

How to get paid as company owner

As company owner or director, you can receive money from the company only through properly documented channels. In practice, this usually means salary or administrator remuneration, invoices for genuine professional services where appropriate, and/or dividends. The company’s money is not your personal money, and personal expenses should not simply be paid from the company bank account. Instead, there are two main ways to withdraw money from the company:

- You pay yourself a salary or invoice the company for your services; and/or

- You withdraw company profits in the form of dividends.

In practice, both options are often combined to optimize tax efficiency (see below).

Tax considerations

Many people choose a company structure to reduce the impact of higher income tax rates. In Spain, personal income tax, or IRPF, is progressive. Using Catalonia as an example, as of 2024, income above €60,000 is taxed at 44%: 22.5% at the state level and 21.5% at the regional level. This increases to 46% for income above €90,000: 22.5% at the state level and 23.5% at the regional level.

Companies, by contrast, are subject to corporation tax. Small companies with an annual turnover below €1 million pay 19% in corporation tax on the first €50,000 of profit and 21% on profits above €50,000. Dividends are then subject to additional taxation as capital income, starting at 19%.

For example, for every euro earned above €60,000, a regular autónomo retains only 63 cents. If that same euro is recorded as company profit, it is first taxed at 19% corporation tax. The remaining amount is then taxed again at 19% when paid out as a dividend, leaving you with approximately 65.6 cents. However, because capital income tax is also progressive, dividend payments between €6,000 and €50,000 are taxed at 21%, meaning that you retain approximately 64 cents from each euro in this range. Even so, high-income earners may pay slightly less tax through a company structure. However, dividends are not completely irrelevant for social security. Although dividends are taxed as savings income for IRPF purposes and are not subject to payroll-style social security contributions, dividends received by an autónomo societario from their company can be included when Seguridad Social determines the RETA income tranche. This reduces the apparent social-security advantage of extracting profits as dividends, especially at higher income levels.

Bookkeeping and tax filings

Operating through a company significantly increases the administrative burden, as separate bookkeeping and tax filings are required for both you, as the autónomo societario, and the company itself. Given the complexity of corporate tax law, many company owners rely on professional accounting services, which creates additional costs. Packages for small companies without employees typically start at around €800 per year.

In addition, invoicing your own company involves VAT and income tax withholdings of 15%, which can affect short-term cash flow because some money is always tied up in VAT and withholding tax, owing to delayed VAT refunds and advance tax payments. This can be particularly noticeable if most of your clients are private individuals or non-Spanish businesses, as regular autónomos do not apply withholding tax to these types of clients.

Dissolving a company

Ceasing operations as a regular autónomo is generally straightforward and cost-free. By contrast, winding down a company involves more extensive paperwork and additional costs, including notary fees.

Is it worth forming a company? The short answer: it depends.

Now that you know a little about what it means to have a company in Spain, let us consider whether it is actually worth your while. This depends largely on why you want to have a company in the first place. Below, we look at three of the most common reasons in turn.

Reason 1: You want to limit your personal liability

For self-employed individuals, personal liability is a significant concern. As a regular autónomo, your personal assets may be at risk for business debts or legal claims. In extreme cases, this could mean putting your savings at risk or even facing personal bankruptcy. By contrast, a limited liability company protects your personal assets from business liabilities. In Spain, the company’s liability is generally limited to its share capital, which must be at least €3,000. However, this protection does not extend to cases of gross negligence or fraudulent conduct by the company’s director.

That said, reducing personal liability does not necessarily require forming a company. Professional risk insurance can be an effective alternative, providing coverage for civil liability and legal assistance in client disputes. A quick online search shows that some insurance companies offer annual liability coverage of up to €150,000 for premiums as low as €238. If your main reason for considering a company structure is to limit your personal liability, professional risk insurance may meet this need with less expense and administrative burden than forming and maintaining a company.

VERDICT: If your primary motivation for forming a company is to limit your personal liability, professional risk insurance may be a simpler and more cost-effective solution.

Reason 2: Your earnings are starting to exceed €50.000 and your accountant has told you that you can pay less tax by forming a company

To evaluate this claim, it is useful to compare the self-employed model — as a regular autónomo — with the company model, in which you operate as an autónomo societario through an S.L.U.

Financial Comparison: Regular Autónomo vs. Limited Company

| Autónomo | Company |

|---|---|

| In this model, you are a regular autónomo. This means that you pay progressive income tax and social security contributions on 100% of your net profit. | In this model, you are an autónomo societario operating through an S.L.U. The company pays you salary or administrator remuneration, and remaining after-tax profits may be distributed as dividends. Salary is taxed in the general IRPF base, while dividends are taxed in the savings base after corporation tax has been paid by the company. For RETA purposes, however, the income calculation for an autónomo societario may include both remuneration from the company and dividends derived from the shareholder’s participation. |

For simplicity, let us consider the case of a single person without dependents or disability who is tax resident in Catalonia.

Example 1: Net profit of €40,000

| Autónomo | Company | ||

|---|---|---|---|

| Income | € 40,000 | Salary you pay yourself* | € 37,150 |

| Income tax (IRPF) | € 7,062.55 | Income tax (IRPF) | € 6,094.81 |

| Social security (SS) | € 5,435.30 | Social security (SS) | € 5,435.30 |

| Civil liability insurance | € 238.00 | Company bookkeeping | € 800.00 |

| Remaining profit in company | € 2850.00 | ||

| Corporation tax on profit (19-21%) | € 541.50 | ||

| Left to take out as dividends | € 2308.50 | ||

| Capital gains tax on dividends | € 438.62 | ||

| Total tax + SS | € 12,497.85 | Total tax (IRPF+Corp.+Cap. gains) + SS | € 12,510.23 |

| NET take home | € 27,264.15 | € 26,689.77 | |

*For the annual net profit above, this is the optimal amount (in terms of NET take home) to invoice your company in Catalonia if you are single, without kids, and without disability.

Example 2: Net profit of €60,000

| Autónomo | Company | ||

|---|---|---|---|

| Income | € 60,000 | Salary you pay yourself* | € 43,750 |

| Income tax (IRPF) | € 13,956.10 | Income tax (IRPF) | € 7862.35 |

| Social security (SS) | € 6,547.07 | Social security (SS) | € 6,547.07 |

| Civil liability insurance | € 238.00 | Company bookkeeping | € 800.00 |

| Remaining profit in company | € 16,250.00 | ||

| Corporation tax on profit (19-21%) | € 3,087.50 | ||

| Left to take out as dividends | € 13,162.50 | ||

| Capital gains tax on dividends | € 2,644.13 | ||

| Total tax + SS | € 20,503.17 | Total tax (IRPF+Corp.+Cap. gains) + SS | € 20,141.05 |

| NET take home | € 39,258.83 | € 39,058.95 | |

*For the annual net profit above, this is the optimal amount (in terms of NET take home) to invoice your company in Catalonia if you are single, without kids, and without disability.

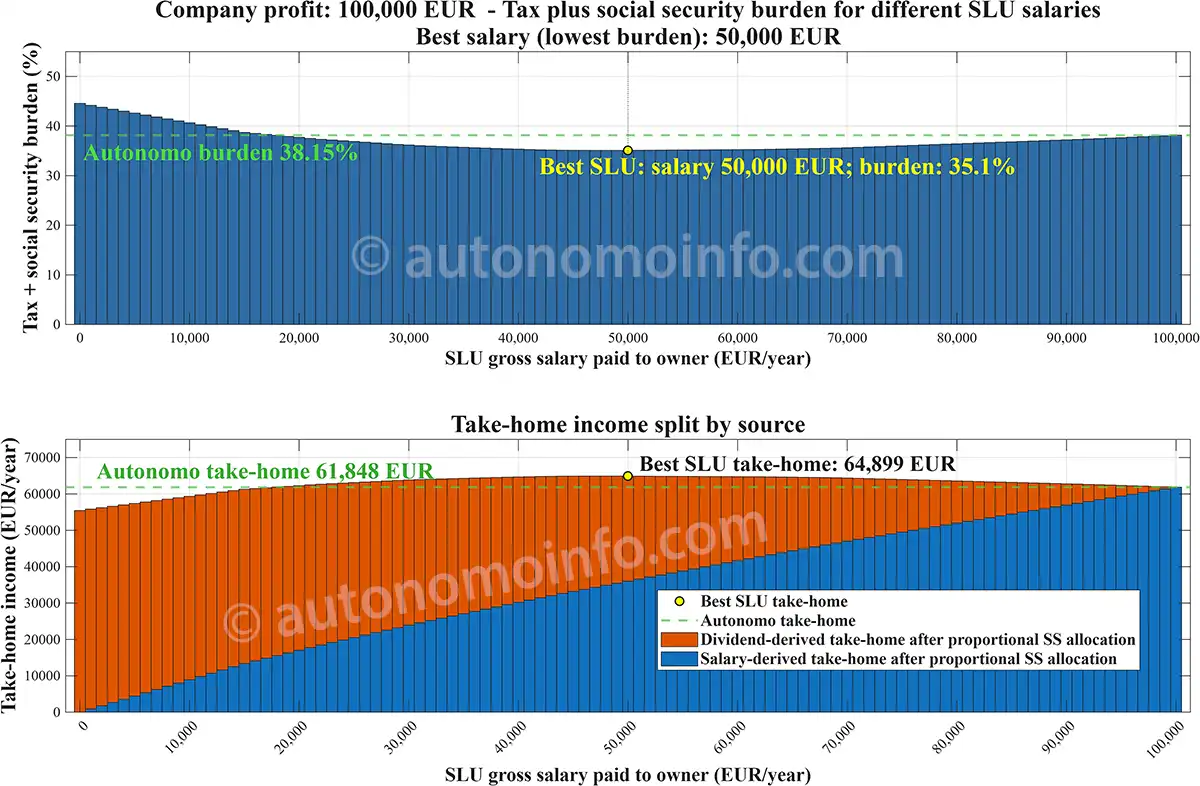

Example 3: Net profit of €100,000

| Autónomo | Company | ||

|---|---|---|---|

| Income | € 100,000 | Salary you pay yourself* | € 50,000 |

| Income tax (IRPF) | € 30,863.67 | Income tax (IRPF) | € 9,928.17 |

| Social security (SS) | € 7,288.22 | Social security (SS) | € 7,288.22 |

| Civil liability insurance | € 238.00 | Company bookkeeping | € 800.00 |

| Remaining profit in company | € 50,000.00 | ||

| Corporation tax on profit (19-21%) | € 9,500.00 | ||

| Left to take out as dividends | € 41,500.00 | ||

| Capital gains tax on dividends | € 8,385.00 | ||

| Total tax + SS | € 38,151.89 | Total tax (IRPF+Corp.+Cap. gains) + SS | € 35,101.39 |

| NET take home | € 61,610.11 | € 64,098.61 | |

*For the annual net profit above, this is the optimal amount (in terms of NET take home) to invoice your company in Catalonia if you are single, without kids, and without disability.

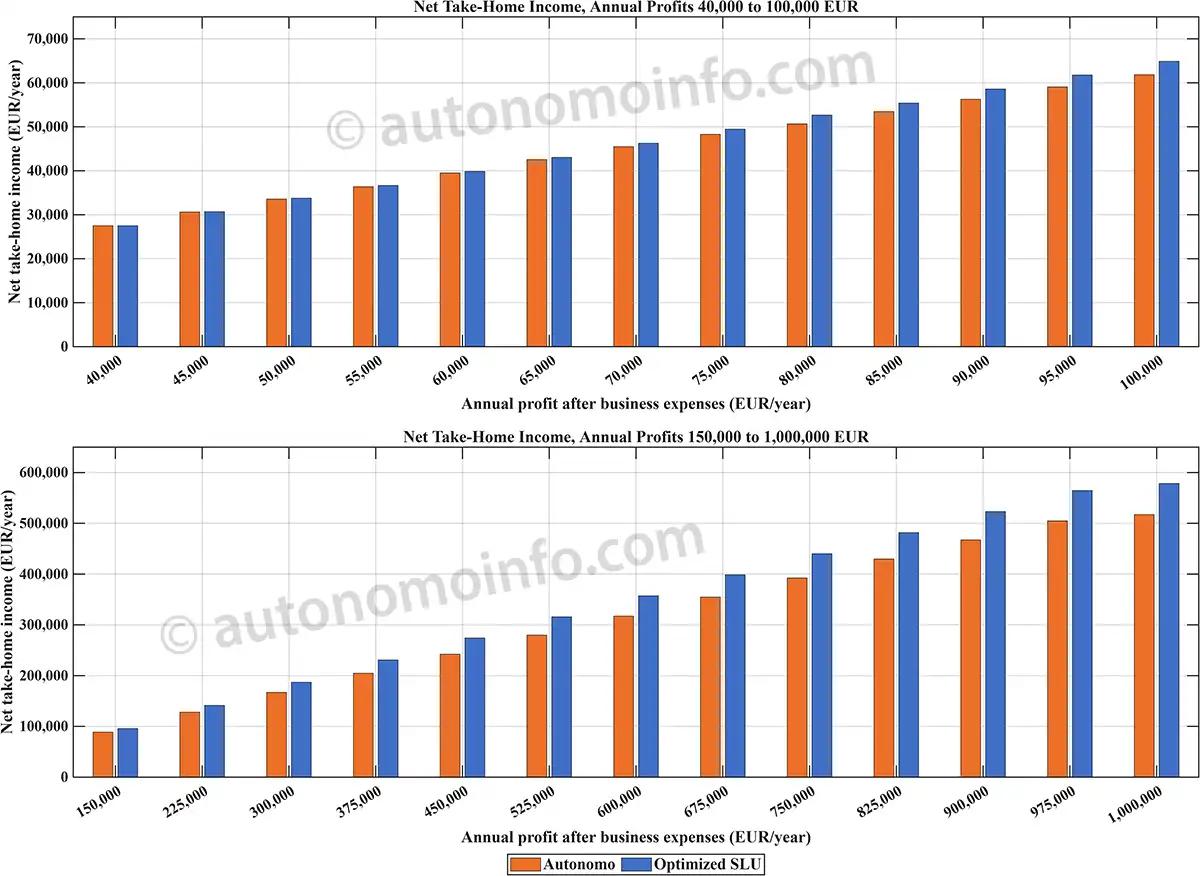

The figure below shows how your NET take home varies for annual profits ranging from €40,000 to €1 million, both as a regular autónomo and a company owner.

Conclusion

In summary, the financial implications suggest that adopting a company structure in Spain provides tangible fiscal benefits only when annual profits consistently exceed €60,000. Even with a substantial profit margin, such as €100,000, the savings on tax and social security contributions remain relatively modest, at just over €2,500 per year. This marginal financial gain must be weighed against the costs of setting up and eventually dissolving a company, the increased administrative burden, and the impact on short-term cash flow due to VAT and withholding tax. In the model shown here, the savings from the company structure mainly come from the interaction between corporation tax, dividend taxation, and the progressive IRPF rates applied to salary. They should not be understood as simply avoiding social security on dividends, because dividends received by an autónomo societario can be included when determining the RETA income tranche. The financial benefit must also be weighed against company setup and dissolution costs, bookkeeping costs, increased administrative complexity, and possible cash-flow effects from tax filings and withholdings.

VERDICT: From a purely financial standpoint, forming a company may not be justifiable for an individual professional in Spain unless profits are well into six figures. Otherwise, the savings are limited and may be offset by potential drawbacks, including reduced future pension entitlements and benefits.

Reason 3: You are trying to attract larger clients who may prefer to deal with companies rather than self-employed individuals

However, the decision to form a company may not depend solely on liability or financial considerations. From a business development perspective, operating as a company may appeal to larger clients or institutions that prefer, or even require, working with corporate entities rather than individual freelancers. Their reasons may range from liability concerns to internal corporate policies. Although a regular autónomo with adequate civil liability insurance may offer sufficient protection, the perceived credibility and professionalism of a company can be advantageous when trying to attract certain clients.

VERDICT: Ultimately, the decision to form a company depends on your personal circumstances, expected revenue, and the strategic value of presenting yourself as a corporate entity. The potential benefits in terms of client perception and market opportunities must be weighed against the increased operational complexity and costs associated with maintaining a company.