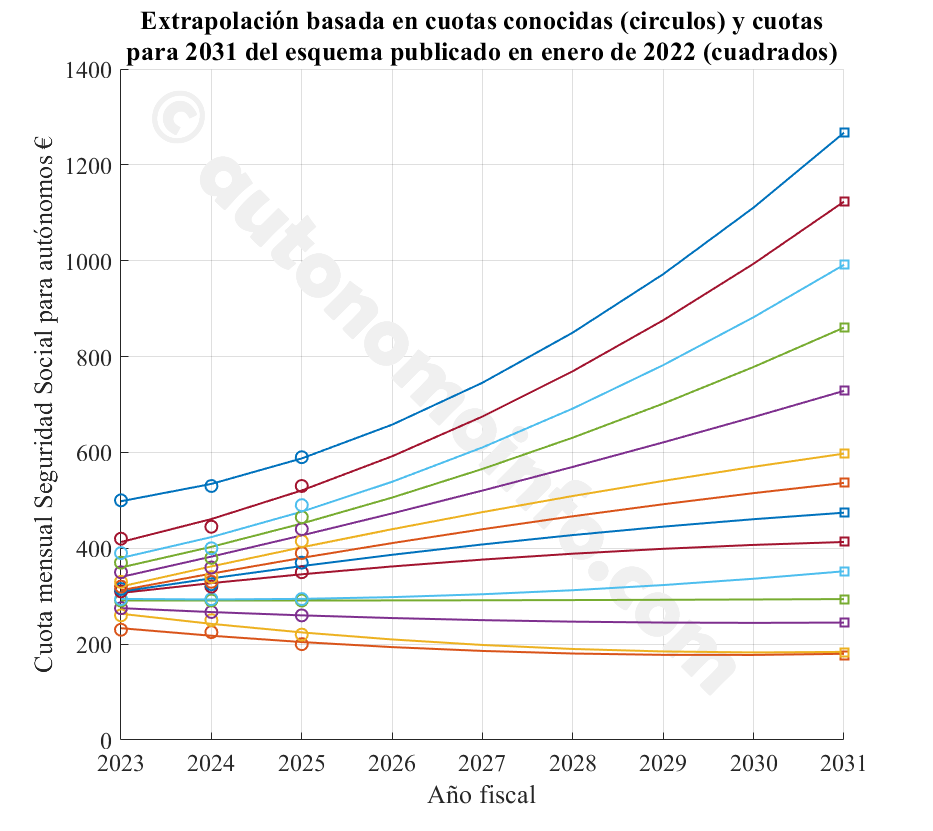

Cómo estimamos las cuotas para 2026-2031

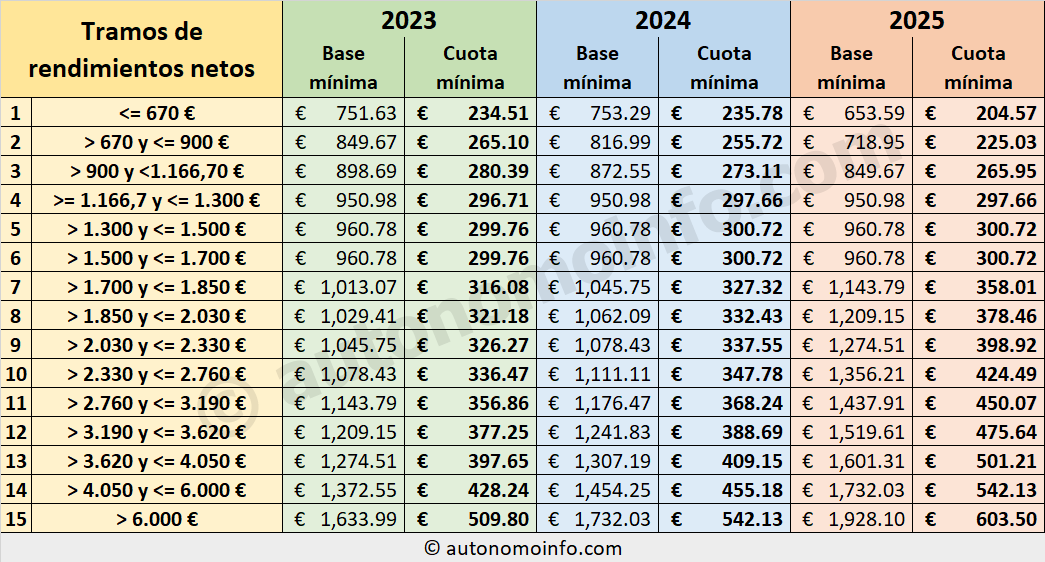

En 2022 el gobierno español ha puesto en marcha un plan para aumentar progresivamente las cotizaciones de los autónomos a la Seguridad Social durante un periodo transitorio de 9 años desde 2023 hasta 2031. Por ahora, el Gobierno solo ha publicado las nuevas cotizaciones para los años 2023-2025, mientras que los valores para los años siguientes no se conocerán hasta 2025. Pese a ello, nuestra calculadora te permite utilizar años fiscales hasta 2031, el último año del período de transición. A continuación te explicamos cómo las estimamos.Antes de que se aprobara el esquema actual, el gobierno ya indicó cómo quiere incrementar las contribuciones hasta 2031. El esquema propuesto por el gobierno fue publicado en un artículo en El País. Si bien este esquema ya ha cambiado, proporciona una indicación de dónde potencialmente llegarían las cotizaciones al final del período de transición en 2031. Con el fin de estimar las contribuciones para los años 2026-2031, usamos los años ya conocidos (2023-2025), usamos las cuotas para 2031 del esquema publicado en El País, y aplicamos una regresión de mínimos cuadrados (mejor ajuste) de una ecuación polinómica de segundo grado para obtener los años intermedios 2026-2030. El resultado se muestra a continuación.

Obviamente, en este momento estos datos son altamente especulativos y solo pretenden proporcionar una indicación de hacia dónde podrían dirigirse las cosas después de 2025.

Calcula tu renta/IRPF y la nueva cuota de autónomos que debes pagar a la Seguridad Social a partir de 2023

Clica para mas información sobre el sistema de autónomos en España

Usa esta herramienta para calcular cuánto tendrás que pagar en contribuciones a la Seguridad Social y en impuestos (IRPF) con el nuevo sistema de autónomos en España introducido en 2023 y cómo esto afecta a tus ingresos netos en comparación con el sistema anterior.